How IFIs Work

The Challenge

The philanthropic space hasn’t changed much over time—it largely consists of a traditional investment corpus that seeks to maximize financial return, with traditional annual grantmaking that seeks to maximize social impact.

The Opportunity

But what if the philanthropists weren't constrained by this one-dimensional tradeoff between returns and impact? Perhaps the investment landscape would look something like this.

In this case, a range of impact-first investments give philanthropists the ability to enjoy grant-style impact while generating investment-style returns. Let's look at some examples.

Growth equity funds for rural businesses provide the capital and support needed to bring good ideas to scale.

Low-interest loan funds for affordable housing help build wealth in lower-income communities.

Recoverable grants for nonprofits are repaid if the recipient organization hits key milestones.

Let’s dig in on some of these details.

“Impact-first investing” (IFI) is a third bucket that provides an additional tool to unlock and deploy capital into innovative and sustainable market-based solutions to our most complex societal challenges. They include everything from loan funds deployed to mission-driven organizations to catalytic first-loss capital to venture investments in impact startups and beyond. Organizations have increasingly relied on impact-first investments to build interventions that become self-sustaining—not reliant on grants—while also having the potential to attract investment capital to scale more quickly.

How the IFI Tool visualizes IFIs

The IFI Tool asks users to consider the overall social impact of their philanthropic asset portfolio: what combination of philanthropic giving, market-rate investments, and impact-first investments generates the outcomes you want — across both impact and financial returns?

Decisions between grantmaking and IFIs ultimately depend on the nature of the specific problem, the goals of the philanthropic investor, and—critically—their assumptions about return and relative impact between a given IFI and a comparable grant.

The critical question is how impact-first investment opportunities trade off impact and financial returns—that is, in what circumstances an impact-first investment’s combination of social impact and financial returns leads to preferred overall outcomes for their portfolio, compared to a conventional strategy limited to traditional giving and market-rate investments.

The IFI Tool is designed to help philanthropic investors navigate these choices—not by prescribing answers, but by provoking thoughtful, assumption-driven analysis of what allocation approach best fits their aims.

Four drivers of impact value creation

Impact-first investments can create value in many different ways. When it comes to comparing that value to that of a grant or donation, here are four factors to consider:

- Capital available to recipient (favors grants): Because investors have a claim on returns, IFIs reduce the share of funds that the recipient of the investment can use to create social value, compared to a no-strings-attached grant to that recipient.

- Risk aversion (favors grants): Investment structures may create incentives for recipients to be more cautious than they would with grant funding, potentially forgoing impact from activities with a perceived higher risk to their ability to repay investors.

- Financial incentive alignment (favors IFIs): Conversely, investment structures can create incentives for additional funder support and greater efficiency than would occur with a grant, by improving recipients’ financial discipline and program sustainability.

- Catalytic leverage (favors IFIs): IFIs can de-risk opportunities and test commercial viability – unlocking commercial capital to scale beyond what is possible with grants alone.

Common Questions

“Impact investing” as a category has grown significantly in recent decades and is currently estimated at $1.57 trillion, but despite these growth numbers there is a gap in a specific type of impact investing: impact-first investing. It is important to distinguish between finance-first impact investing (or market-rate impact investing) and impact-first investing. In the case of finance-first impact investing, investors seek to allocate capital to ventures and projects that make an impact while still ensuring risk-adjusted market-rate returns; indeed, 74 percent of impact investors state that they target market-rate returns. This type of investing has grown significantly, driven in large part by private equity firms seeking out companies that have a more intentional focus on societal and environmental impact. While this concept—shifting a portfolio toward more impactful investments where possible while still maintaining the same returns—has an important role, it excludes a huge array of critical projects that have below-market risk-adjusted expected returns, in some cases because of their unproven models and in others because their specific impact goals preclude higher returns.

Most impact investing falls into the broader category of market-rate investing; impact-first investing prioritizes social or environmental impact, expecting a risk-adjusted below-market-rate return. That said, impact-first investing differs from philanthropic giving—which is donating money for charitable purposes without expectation of repayment or financial return; the funds are deployed once and not recovered, generating what is effectively a negative 100% return. Impact-first investments may at times generate significant returns, but investors take on a higher level of risk in pursuit of impact objectives—especially as they often deploy capital to initiatives that are unable to attract traditional investors.

IFIs are critical because there are increasingly innovative and sustainable market-based solutions that generate some level of financial return—just not market-rate returns. Because of the limited adoption of impact-first investing, these solutions are frequently misunderstood by both philanthropists and investors—even impact investors.

There are many types of impact-first investments (IFIs). You can click here to view a few case studies to learn more. Meanwhile, below are a few types of impact value creation that IFIs—depending on the category—can generate.

- Redeployment: As noted, the redeployment—or recycling—of capital is a defining characteristic of IFIs. It can significantly extend impact. For instance, below-market interest rate loan funds that deploy capital to underserved students (and generate some return) can ultimately reach many more students than grants (which have a negative 100% return). The repaid loan funding from the initial cohort of students is recycled to serve more cohorts of students on an ongoing basis without infusing more capital—whereas a grant can only fund one cohort unless more grant funding is added.

- Note: when it comes to the IFI Tool, the redeployment effect is explicitly modeled, whereas the other forms of impact value creation should be factored into the user-selected “Impact Relative to Philanthropic Giving” variable.

- Social multiplier: Impact-first investments can act as a social multiplier. In many cases, the expected financial returns of such an investment are below-market rates, but the expected social impact is significantly greater than the financial value captured. An example here is an early-stage venture fund focused on public health interventions. Limited seed investments can be critical to the launch of an impact startup that ultimately generates transformative, outsized results on health outcomes—one whose total value to society significantly outweighs any financial profit the venture generates.

- Financial incentives: IFIs may create stronger financial incentives than grants. A loan, for example, encourages the borrower to achieve sufficient financial success to repay it. It also incentivizes the investor to monitor and support the borrower. For instance, a below-market interest loan fund to early-stage nonprofits can incentivize the organization to build a sustainable, revenue-generating model—leading to a more stable and lasting impact than might be achieved with grant funding alone.

- Social incentives and alignment: Impact-first investments can also foster stronger social incentives and alignment compared to market-rate investments. For example, impact-first private equity or venture capital funds—or direct investments in social impact-driven businesses—allow mission-aligned investors to support companies in balancing financial performance with social goals. This alignment can influence follow-on investments and support mission-preserving exits.

- Catalytic structure: Impact-first investments can be catalytic in their structure, attracting additional capital into a project or fund. For example, an investor taking a junior position—such as subordinated debt, equity, or a guarantee—can attract more traditional capital in senior positions. This structure amplifies the total capital invested in the initiative. Unlike a grant, an investment provides returns and aligns incentives: the impact-first investor is motivated to select and monitor projects for financial performance, benefiting senior investors while supporting the project’s impact goals. An example is the SDG Loan Fund, where FMO Investment Management and the MacArthur Foundation collectively pledged $136 million in “first-loss capital” that catalyzed the closing of a $1.1 billion fund from institutional investors.

- Catalytic for investees: IFIs can also catalyze follow-on capital directly into the specific project at hand. For instance, impact-first venture investments into early-stage impact startups can help attract traditional venture capital later on—once the venture has proven the ability to establish a fast-growing revenue model.

- Catalytic for category: Impact-first investments in a specific technology, geography, sector, or business model can de-risk and build infrastructure for that category, attracting future financial investment. For example, successful early investments in microfinance helped establish the category and drew in traditional capital over time.

- Catalytic for public investment: Finally, IFIs can also catalyze public sector investment. In this case, the uncertainty addressed by the IFI can involve both the program’s public fit and financial sustainability. Demonstrating that a model can deliver impact while covering part of its costs can make it more appealing for government adoption, as it raises the social return on investment and reduces fiscal burden. Structuring philanthropic capital to mirror the desired public program—for instance, using a philanthropic loan fund to model government-subsidized community loans—can generate stronger evidence on costs and outcomes, building a clearer case for public or blended funding.

For impact-first investment strategies, investors prioritize greater social impact — so they are typically willing to accept below-market financial returns in exchange for achieving it.

One key consideration is timing: Instead of quick financial gains or immediate impact impact-first investments often prioritize patient capital, allowing their investees time to grow and create lasting change. Financial returns may be slower or smaller, but the long-term impact is the primary goal.

We know that this is not an easy question to answer: not all problems have investible solutions, and not all impacts look the same.

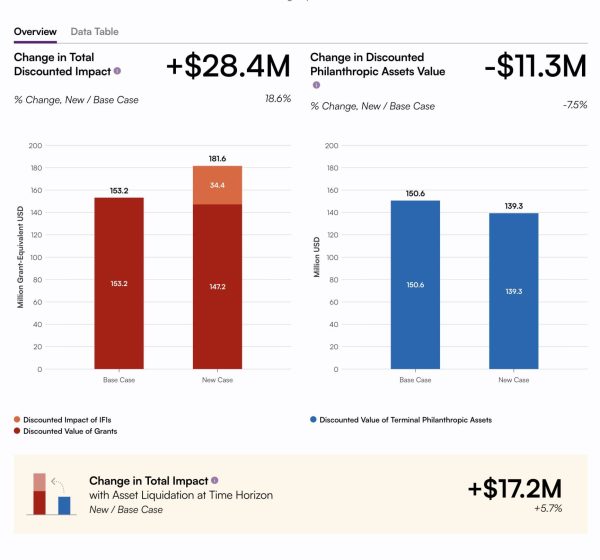

The IFI Tool acknowledges these tensions by focusing on portfolio-level analysis rather than head-to-head comparisons. The relevant question becomes: “given my portfolio as a whole, what is the relative impact of the dollars I allocate to grants versus impact-first investments?” Your input for this assumption allows the IFI Tool’s model to express all impacts in “grant-equivalent” dollars, thus enabling apples-to-apples comparisons between the impacts and financial returns of the base case (no IFIs) and the new case (inclusive of IFIs).

To set your initial assumptions about the impact of a portfolio with IFIs relative to grants, we recommend starting by looking at some examples – you can find several in the Case Studies – and experimenting with different inputs. The IFI Tool allows you to explore a range of plausible values and observe how your results change in real time, highlighting which assumptions might be worth a closer look.